What does the future hold

for UK equities?

Sponsored by

The question What does the future hold for UK equities? kicked off a lively debate from our panel of experts and watching subscribers as part of our Investor Day event, as the experts got to grips with some of the features and quirks of the UK market that have emerged over the past couple of years .

Our experts, Joachim Klement, Head of Equity Strategy at Liberum, Simon Gergel, Chief Investment Officer UK Equities at AllianzGI and Portfolio Manager of The Merchants Trust and Heloise Greeff, a Champion Level Investor at eToro, all agreed that the outlook for UK equities would be challenging but also offer many opportunities for private investors.

UK indices have proved to be an exceptionally solid investment proposition over the past few months, in contrast to more garlanded, but flashier indices (for this read the Nasdaq) that have taken a proverbial swan dive into bear market territory. The question for our experts was straightforward, how would the index perform and what should investors look out for?

The question for our experts was straightforward, how would the index perform and what should investors look out for?

The key lessons learned

To begin to answer that question, we had to go over the most important investment lessons from the past couple of years. Simon Gergel said: “It has been an extraordinary couple of years. We couldn’t have seen the pandemic coming, or the war in Ukraine, but overall, what the period has taught us is that valuation still matters, and that money is not free forever.”

Joachim Klement said: “The ability to look past the next couple of months is going to be key to how investors should react. Equity markets in the long run are a good deal more resilient than the situation currently implies.” Heloise Greef agreed with that point and added that investors cannot allow their emotions to dominate their actions. “However, we have also seen the rise of a new generation of retail investors who through their coordinated, or uncoordinated, efforts have been able to influence the market and bring previously untapped capital to bear,” she said.

The British exception?

Some of the resilience of UK equities is down to the inherent features of the market. “One of the things about the FTSE All-Share is that it is naturally very international, about 70 per cent of sales are generated abroad. In addition, we have some of the highest standards of governance… There has been some uncertainty over Brexit, which has affected valuations,” said Gergel.

The other simple fact, as Greef pointed out, is that the UK has very few inflated valuations: “The UK is not well known for its technology companies… instead it has a weighting towards finance and natural resources – the giants like HSBC and Shell – and while that has been a drag over the past couple of years for UK investors, on the other hand, that hasn’t necessarily been a bad thing, as this has shielded investors from the rotation away from growth stocks,” she said.

The UK is not well known for its technology companies… instead it has a weighting towards finance and natural resources

“There is nothing wrong with getting rich slowly,” said Klement: “We learned the benefits this year of stable compounders. The UK market is not the most dynamic, but it is also not going down the most in a recession. We have companies that are essentially global companies and earn a lot of their revenues in US dollars.” Klement argues that dollar-earning companies have an inherent buffer in their top-line revenues from a strengthening dollar when times are tough.

He added that the European equities have a different type of exposure that tends to bring out the strengths of the UK market. “Companies in Germany and France, for instance, will have far greater exposure to China and with Chinese growth slowing down that makes, at the moment, for a better outlook for the UK. However, it is still the case that the ‘Sword of Damocles’ hangs over Europe because of its reliance on Russian natural gas. The UK is partly self-sufficient in this context, so seems to have a better position,” Klement said.

The outlook for dividends

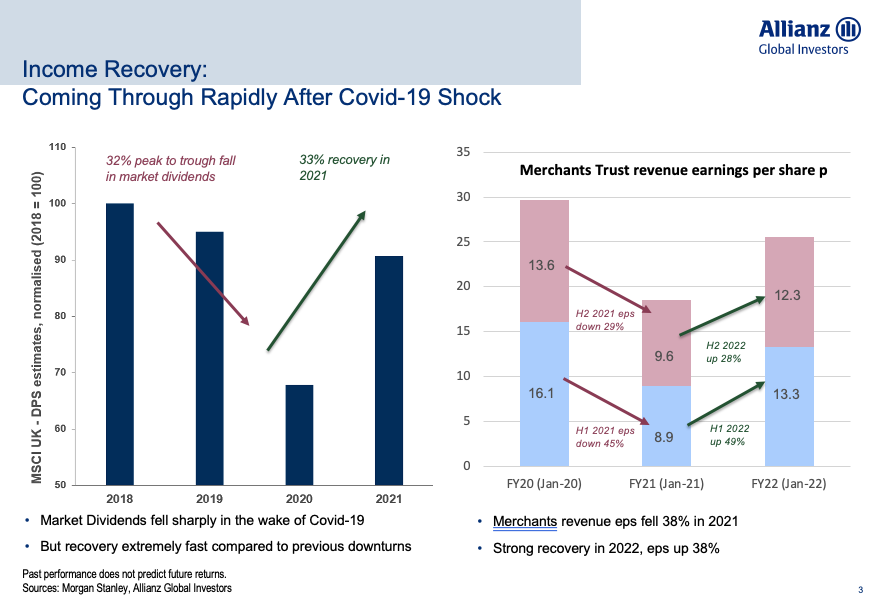

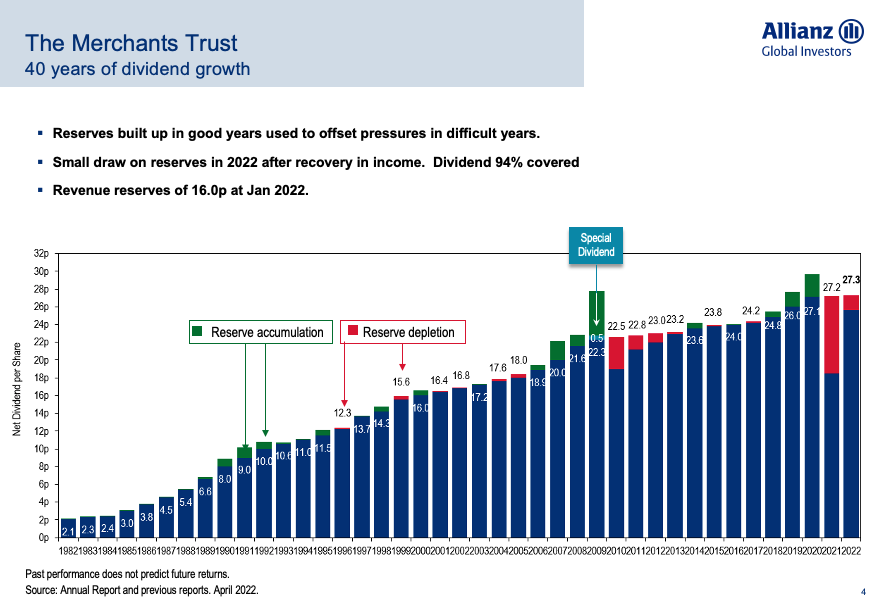

For some investors dividends are an integral part of investing and the UK market also scores highly in this regards with our experts. “I’m an income investor myself,” said Gergel, “and there is a real culture of dividend payouts in the UK that isn’t really the case in America. We have seen a rapid recovery after some of the deepest cuts that I have seen. There are concerns over the economy but we haven’t seen many dividend cuts, though we have to keep this under review. Also, inflation might not be bad for nominal dividends, though gaining a real return might be difficult,” he said.

Joachim Klement said that the development of higher dividend cover was a one feature that had come out of the pandemic period. Free cash flow, particularly from resources companies benefiting from high prices is a trend that the UK market that benefits from, and “A lot of UK businesses are run for income,” he said.

Main predictions

Heloise Greef said that many UK companies have many areas in which they excel – cyber security, energy transition, life sciences. There is also scope for the old economy businesses to reinvent themselves, players like Drax, for instance, shifting towards renewables and carbon capture technology.

Joachim Klement was ebullient about the outlook for the next three to five years – on a sector adjusted-basis the UK market is the cheapest of the major indices. The major problem is the next 12 to 18 months where investors must reach the point of maximum pessimism before deciding to return to the market in greater numbers, he said.

Simon Gergel said: “It is difficult to make predictions, especially about the future.” The valuations in the UK are interesting, with large gaps emerging between high growth and better value mature businesses. For instance, the financial sector is offering a lot of opportunities and a stock picking strategy would yield better results than a passive investing approach as the low liquidity at individual company level is causing large swings in price, offering a bargain opportunity, he said.

“It is difficult to make predictions, especially about the future”

For more video content from this event see the following articles:

Future of Private Investing: Inflation's effect on your investments

Future of Private Investing: How far can the Bank of England go?

Sponsored by